Stakeholders and Stakeholder Activism

- Pressure to Incorporate Stakeholder Interests

- Legal and Economic Implications

- Director and CEO Views on Stakeholders

- ESG Metrics and Disclosure

- External Assessment of ESG

A corporation should exist not only to increase value for shareholders but also to address the needs of other (non-shareholder) stakeholders. These stakeholders include employees, trade unions, customers, suppliers, local communities, and society.

Save 35% off the list price* of the related book or multi-format eBook (EPUB + MOBI + PDF) with discount code ARTICLE.

* See informit.com/terms

This chapter is from the book

This chapter is from the book

This chapter is from the book

The governance mechanisms discussed in this book so far have been considered from a shareholder-centric perspective. A fundamental premise throughout is that the primary purpose of a corporation is to create value for shareholders and the obligation of a board is to ensure this purpose is achieved. Chapter 3 outlines board operations and fiduciary duties from this standpoint. Chapter 6 evaluates strategy development and risk management with this objective in mind. Chapter 11 accepts the premise that an effective market for control facilitates the transfer of corporate assets to owners who will derive the highest value from them. Many of the empirical studies discussed in this book measure the effectiveness of governance mechanisms by their impact on shareholder value and corporate profitability, and the central definition of corporate governance that we employ—that a separation between the ownership of a company and its management creates opportunity for self-interested managers to take actions that benefit themselves at the expense of shareholders—is rooted in the premise that preserving shareholder value is a primary objective.

An alternative viewpoint, however, exists—that a corporation should exist not only to increase value for shareholders but also to address the needs of other (non-shareholder) stakeholders. These stakeholders include employees, trade unions, customers, suppliers, local communities, and society. In this chapter, we turn to this issue. We start with an overview of the pressures that corporate managers face to incorporate stakeholder objectives into their planning, including pressures that come from their own shareholder base. We discuss the legal and economic implications of a stakeholder-centric governance model, including its potential impact on strategy, risk, and value creation. Then we examine how corporate managers and directors view their obligations to stakeholders, and discuss the recent trend of CEO activism on social issues. We end with a discussion of the metrics used to track a corporation’s progress toward achieving social goals—including those developed by third-party rating providers—and their effectiveness.

As we will see, managing a corporation from a stakeholder perspective is not a simple undertaking and highlights a fundamental tension that has long existed in corporate boardrooms: how to balance competing interests to ensure the success of the organization over the long term.

Pressure to Incorporate Stakeholder Interests

In 1970, economist Milton Friedman famously argued that a company’s only social responsibility is to maximize shareholder value. He argued that corporate executives are employed by the owners of the firm (shareholders) and their obligation is to manage the business in accordance with the wishes of their employer—that is, to increase its value under the constraints of the law and accepted ethical standards. When other purposes are added to the equation, they require trading off this objective by diverting resources to a purpose that the owners of those resources have not approved, with the cost borne by shareholders through lower profit, customers through higher prices, and workers through lower wages and employment.1

Despite Friedman’s argument, pressure has grown on large, publicly traded firms to incorporate stakeholder interests into their long-term planning. Without providing an exhaustive list, stakeholders include employees of the firm, customers, suppliers, creditors, trade unions, local communities, and society at large. The interests of these groups are broad and include environmental sustainability, reduction in waste or pollution, higher wages, workplace equality, diversity, providing access to groups who cannot afford products or services, and being a responsible counterparty or local citizen. Because companies operate in different industries, stakeholders and stakeholder interests differ across corporations. When we talk about stakeholder interests, we generally refer to the most directly relevant issues—such as climate change for energy producers, product waste for goods manufacturers, or affordability for healthcare providers. In some cases, the social interest is assumed to be common across companies, one example being diversity.

Various labels have been applied over time to describe corporate and investor efforts to address stakeholder needs. These include socially responsible investing (SRI), corporate social responsibility (CSR), and environmental, social, and governance (ESG).

Pressure for corporations to address stakeholders’ interests has come from multiple fronts:

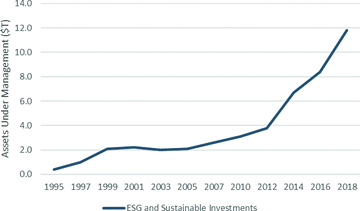

Money flowing into sustainable investment funds—In 1995, less than $1 trillion was invested with money managers and institutional investors dedicated to sustainable, responsible, and impact investing in the U.S. By 2018, that number exceeded $12 trillion (see Figure 13.1).2

Source: U.S. SIF Foundation, “Sustainable and Impact Investing—Sustainable Investing Basics (2018).

FIGURE 13.1 Sustainable and responsible investing in the U.S.

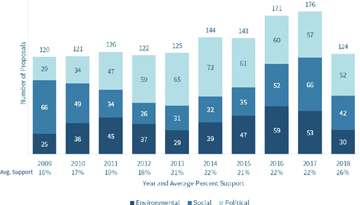

ESG-related proxy proposals—The number of shareholder-sponsored proxy proposals relating to ESG considerations has generally increased in time and the percent of shares voted in favor of these proposals has also increased (see Figure 13.2).3

Note: The decline in shareholder-sponsored proxy proposals in 2018 was the result of higher direct engagement between companies and sponsoring shareholders.

Source: FactSet. Calculations by the authors in David F. Larcker, Brian Tayan, Vinay Trivedi, and Owen Wurzbacher, “Stakeholders and Shareholders: Are Executives Really ‘Penny Wise and Pound Foolish’ About ESG?”

FIGURE 13.2 Shareholder-sponsored proxy proposals on ESG-related topics.

Institutional investors—Large institutional investors that had previously taken passive stances on ESG-related issues have become more assertive. For example, each of the “Big Three” index funds—BlackRock, Vanguard, and State Street Global Advisors—have engaged in advocacy campaigns in recent years to shape the governance practices of their portfolio companies in areas relating to social responsibility. (We discuss this more fully later.)

ESG metrics—Data providers use survey data and publicly observable metrics to rate companies along a variety of stakeholder dimensions. This data is sold to institutional investors to inform investment decisions or is used in magazine rankings. Examples of data providers include MSCI, HIP (“Human Impact + Profit”), and TruValue Labs. Examples of published indices include Barron’s 100 Most Sustainable Companies, Bloomberg Gender Equality Index, Ethisphere Institute’s Most Ethical Companies, and Newsweek Top Green. The Sustainability Standards Board (SASB) has tried to standardize the reporting of these metrics. (We discuss ESG measurement more fully later and in Chapter 14.)

Employee activism—Employees of some companies have become more vocal expressing their views to management on environmental or social issues. Social media and internal corporate communications platforms have facilitated this process. Employee activism has forced companies to change corporate policy, withdraw from commercial activities, and take public stances on societal issues about which the company might traditionally remain silent (see the following sidebar).

)

)

Of these sources, institutional investors have played a particularly prominent role promoting stakeholder interests. Beginning in 2014, Vanguard launched a program of direct engagement with portfolio companies to discuss governance-related topics. It dubbed this program “quiet diplomacy.” Vanguard subsequently included ESG criteria in this effort.7 In 2017, State Street Global Advisors launched what it called the “Fearless Girl” campaign to advocate that its portfolio companies increase the number of women on their boards.8

BlackRock has been the most vocal of the Big Three investors to advocate that companies give greater consideration to stakeholder interests. For the last several years, BlackRock CEO Larry Fink has written an annual letter to the CEOs of the companies in BlackRock’s investment portfolio, encouraging them to address a variety of stakeholder-related issues. In 2016, he advocated they lay out “a strategic framework for long-term value creation” and stated that “generating sustainable returns over time requires a sharper focus not only on governance, but also on environmental and social factors.”9 The next year, he encouraged greater attention to “long-term sustainability” and discussed such topics as globalization, wage inequality, tax reform, and a more secure retirement system for workers.10 In 2018, he argued that a company needs to have a “sense of purpose” that serves all stakeholders and that “to prosper over time, every company must not only deliver financial performance but also show how it makes a positive contribution to society.”11 In 2019, he argued that “purpose and profit are inextricably linked” and that purpose is “the animating force” to create stakeholder value.12 In 2020, he announced that BlackRock was putting “sustainability at the center of our investment approach” and asked companies to disclose more information on their sustainability efforts, including climate change.13

Because of BlackRock’s size and ownership stake, it is positioned to influence corporate practice: In 2018, it held more than 7 percent of the equity value of the Russell 3000 Index and had an ownership position greater than 5 percent in almost every company in the S&P 500 Index (see the following sidebar).14

In response to pressure from these sources, more than 180 CEOs affiliated with the Business Roundtable agreed to revise the association’s statement on the purpose of a corporation, to emphasize a commitment to all stakeholders and not just shareholders. According to the association:

Since 1978, Business Roundtable has periodically issued Principles of Corporate Governance that include language on the purpose of a corporation. Each version of that document issued since 1997 has stated that corporations exist principally to serve their shareholders. It has become clear that this language on corporate purpose does not accurately describe the ways in which we and our fellow CEOs endeavor every day to create value for all our stakeholders, whose long-term interests are inseparable.

Under the revised statement, association members commit to:

Delivering value to our customers. We will further the tradition of American companies leading the way in meeting or exceeding customer expectations.

Investing in our employees. This starts with compensating them fairly and providing important benefits. It also includes supporting them through training and education that help develop new skills for a rapidly changing world. We foster diversity and inclusion, dignity and respect.

Dealing fairly and ethically with our suppliers. We are dedicated to serving as good partners to the other companies, large and small, that help us meet our missions.

Supporting the communities in which we work. We respect the people in our communities and protect the environment by embracing sustainable practices across our businesses.

Generating long-term value for shareholders, who provide the capital that allows companies to invest, grow and innovate. We are committed to transparency and effective engagement with shareholders.17

We discuss the implications of this commitment next.